Why Market Timing Fails: What Investors Need to Know

Market timing is defined as the practice of moving in and out of the market to avoid losses and capture gains based on short-term predictions. It fails because investors must make two perfect decisions, not one: when to exit and when to re-enter, in markets that are fundamentally unpredictable. The DALBAR 2025 report shows the average equity investor earned 9.24% per year over 20 years ending 2024, compared to 10.35% for the S&P 500. That gap compounds into a significant wealth shortfall over time. Behavioral finance research confirms that cognitive biases like loss aversion make the problem worse, not better.

Why market timing fails: the core evidence

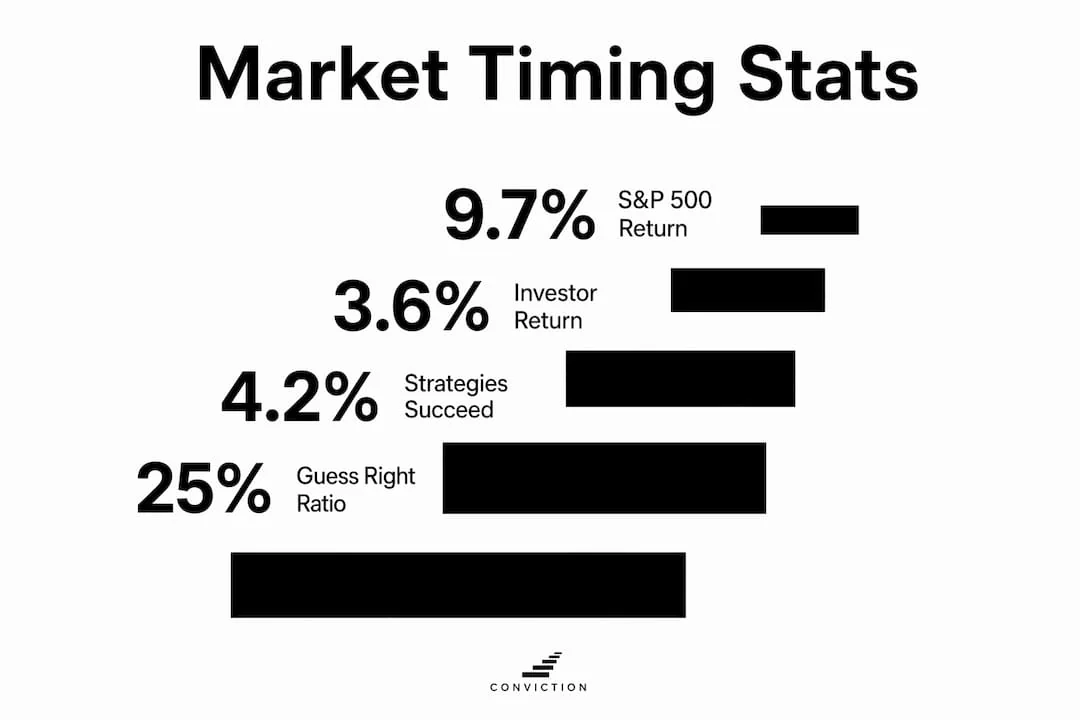

The performance record against market timing is clear and consistent. Historical data through 2022 shows the average equity fund investor earned just 3.6% annually, compared to 9.7% for the S&P 500 over the same 30-year period. That is a 6.1% annualized gap, which means a $100,000 investment grew to roughly a fraction of what a simple index fund would have produced.

Dimensional Fund Advisors tested 720 different market timing strategies in simulation. Only 30 showed any outperformance, and even those results were transient and statistically indistinguishable from random chance. A success rate below 4.2% means timing strategies fail more than 95% of the time.

The table below shows how different investor groups have performed historically:

| Investor group | Approximate annualized return (30 years) |

|---|---|

| S&P 500 index | 9.7% |

| Average equity fund investor | 3.6% |

| Average equity investor (20 years, DALBAR 2025) | 9.24% |

| S&P 500 (20 years, DALBAR 2025) | 10.35% |

The pattern is consistent across time periods. Investors who attempt to time the market consistently earn less than those who simply stay invested.

One reason the gap is so large is the clustering of best and worst market days. The best market days often cluster near the worst days, meaning investors who exit during a downturn frequently miss the sharpest recoveries. Missing just a handful of the best trading days in a decade can cut long-term returns dramatically. You cannot avoid the bad days without risking the best ones.

What psychological factors cause timing to fail?

Behavioral finance identifies several specific biases that make market timing attempts predictably poor. These are not personality flaws. They are wired-in human responses that affect nearly every investor.

Loss aversion. Investors feel losses roughly twice as acutely as equivalent gains. This asymmetry pushes investors to sell during downturns to stop the pain, locking in losses at exactly the wrong moment.

Illusion of control. Switching to cash during volatility feels like a decision, not a retreat. That feeling of control is misleading. Cash is an active investment choice with negative expected value versus equities over the long term.

Panic selling and hesitation. After selling, investors hesitate to re-enter because the market still feels risky. By the time confidence returns, much of the recovery has already happened.

Confirmation trap. Investors seek out news that confirms their decision to stay out. The confirmation trap causes retail investors to re-enter too late, after the bulk of the rebound has already occurred.

Emotional decision-making. Volatile markets trigger emotional responses that override rational analysis. A 10% drop feels like a crisis even when long-term fundamentals have not changed.

These biases do not cancel each other out. They compound. Loss aversion triggers the exit. The illusion of control justifies staying out. The confirmation trap delays re-entry. The result is a cycle that reliably reduces returns.

Pro Tip: When you feel the urge to sell during a market drop, write down the specific reason and the price target at which you would re-enter. This forces you to confront the second decision, not just the first, and often reveals how speculative the timing attempt really is.

Why retail investors lose against institutional traders

Market timing is not just hard. It is structurally disadvantaged for retail investors. Institutional algorithms act on new information before retail investors can read a headline. By the time a news story reaches your phone, the market has already priced in the information.

This creates a systematic disadvantage that no amount of research or discipline can fully overcome. Consider what successful market timing actually requires:

Correctly identifying when to exit before the decline

Selecting an appropriate holding asset while out of the market

Deciding when to re-enter before the recovery accelerates

Managing the tax consequences of the trades

Maintaining the emotional discipline to execute all four steps consistently

Most retail investors fail to get even one of these decisions right consistently. Getting all five right, repeatedly, is not a realistic expectation.

The forward-looking nature of markets makes this worse. Markets price in information before news is widely available, which means the market has already moved by the time a retail investor acts. A headline reading “Markets fall on recession fears” describes something that happened, not something that is about to happen. Acting on that headline means you are already late.

Staying in cash to time market movements also carries a hidden cost. Cash typically lags both inflation and equity market growth over long periods. Every day you sit in cash waiting for the “right” moment is a day your money is not compounding.

What investment approaches actually outperform timing?

The evidence points clearly toward time in the market rather than timing the market. Long-term investors who stay invested through volatility benefit from compound growth, dividend reinvestment, and the full capture of recovery days that market timers miss.

Stay invested through volatility. The S&P 500’s long-term average return rewards patience. Compound growth requires time, and interrupting that compounding with cash positions destroys the math.

Use disciplined portfolio rebalancing. Rebalancing on a schedule, quarterly or annually, forces you to buy assets that have fallen and trim those that have risen. This is a structured, less risky alternative to timing attempts that still responds to market movements without requiring perfect prediction.

Make regular contributions. Dollar-cost averaging, contributing a fixed amount on a regular schedule, removes the timing decision entirely. You buy more shares when prices are low and fewer when prices are high, automatically.

Set a long-term asset allocation. Deciding in advance what percentage of your portfolio belongs in equities, bonds, and other assets removes the emotional pressure to react to short-term market moves. Your allocation becomes your strategy.

Disciplined rebalancing and long-term investing are not passive or lazy approaches. They are evidence-based strategies that consistently outperform the speculative alternative.

Pro Tip: Write down your investment thesis and your target allocation before markets open on any given day. When volatility hits, your written plan becomes your anchor. Investors who have a documented strategy are far less likely to make emotional timing decisions.

Key takeaways

Market timing fails because it requires multiple perfect decisions in unpredictable markets, while behavioral biases and institutional speed make consistent success nearly impossible for retail investors.

| Point | Details |

|---|---|

| Performance gap is large | Average equity investors earned 3.6% vs. 9.7% for the S&P 500 over 30 years. |

| Timing success is rare | Fewer than 4.2% of 720 tested timing strategies showed any outperformance. |

| Biases compound the problem | Loss aversion, confirmation trap, and panic selling create a cycle that reliably reduces returns. |

| Retail investors are structurally disadvantaged | Institutional algorithms price in information before retail investors can act. |

| Time in the market wins | Staying invested, rebalancing regularly, and contributing consistently outperforms timing attempts. |

The emotional pull of timing, and why it keeps drawing investors in

I have talked with a lot of investors over the years, and the pattern is always the same. Nobody thinks they are speculating. They think they are being smart. They watched the news, they saw the warning signs, and they made a calculated decision to protect their money. That feeling is real. The problem is that the market does not care how calculated the decision felt.

What I find most telling is the DALBAR “Guess Right Ratio.” In 2024, it sat at just 25%. That means even in a year when investors had access to more financial information than any previous generation, they called the market correctly only one time in four. That is not a skill gap. That is a structural problem with the strategy itself.

The hardest thing to accept is that doing nothing is often the right move. When markets drop 15%, every instinct says act. The data says stay. That tension never fully goes away, even for experienced investors. What changes with experience is your ability to recognize the feeling for what it is: a bias, not a signal.

The investors I have seen build real wealth are not the ones who called the 2020 bottom or sold before the 2022 correction. They are the ones who stayed invested, kept contributing, and did not let volatility rewrite their strategy. Patience is not passive. It is a deliberate choice made against strong emotional pressure.

— Andi

Build investing confidence without relying on timing

Understanding why timing fails is the first step. The next step is building the knowledge and habits that make disciplined investing feel natural, not forced.

Conviction is an educational platform built around exactly this challenge. Its bite-sized, interactive lessons cover behavioral finance, risk management, and long-term investing principles in a way that is clear and accessible for every level of investor. You will learn how to recognize your own biases, build a strategy grounded in evidence, and stay confident when markets get noisy. If you are ready to invest with clarity and conviction, start learning today and see what a structured investing education actually feels like.

FAQ

Why does market timing fail for most investors?

Market timing fails because it requires multiple correct decisions in unpredictable markets, while behavioral biases like loss aversion and the confirmation trap cause investors to exit too late and re-enter too late.

What does the data say about market timing vs. buy and hold?

The average equity fund investor earned 3.6% annually over 30 years, compared to 9.7% for the S&P 500. Buy-and-hold investors consistently outperform those who attempt to time the market.

How many market timing strategies actually work?

Out of 720 timing strategies tested in simulation, fewer than 4.2% showed any outperformance, and those results were statistically indistinguishable from random chance.

Is staying in cash a safe alternative to being invested?

No. Cash is an active investment choice with negative expected value versus equities over the long term, as it typically lags both inflation and market growth.

What is the best alternative to market timing?

Staying invested through volatility, making regular contributions, and rebalancing on a fixed schedule consistently outperforms timing attempts and removes the need for perfect market prediction.